Written By Jeffery Cartwright and Lawrence Allen | 15 min read

The great global recession of 2008 resulted in a precipitous decline in demand for exports from China. The Chinese Academy of Social Sciences described the impact: “China’s economic growth is over-dependent on the growth of net exports. In 2008, its export-to-GDP ratio reached 32%… with labour-intensive export industries absorbing non-skilled workers from rural areas.”

This article will offer and examine strategies and tactics for Mexico winning its share of the global manufacturing pie through successfully regionalizing manufacturing from far-flung locations such as China. It will present knowledge and perspective that will enable business leaders to better understand the vulnerabilities and capabilities of both China and themselves—relative to the opportunities. It will provide an understanding of where China is in its modern industrial revolution and the actions it is likely to take to retain and continue to attract manufacturing to its shores. And it will analyze Mexico’s strengths and weaknesses in terms of manufacturing, but also its ability to “think global and act global” at the governmental, corporate leadership and cultural levels.

Of concern were shuttered factories idling hundreds of thousands of contract workers en masse, who were originally brought from remote country-side villages by labor scouts to work on year-long contracts in manufacturing cities like Shenzhen. The situation posed serious risk of domestic unrest, so much so that government representatives were deployed with vouchers, busses, military transport and train passes to move idled workers back to their rural hometowns as quickly as possible.

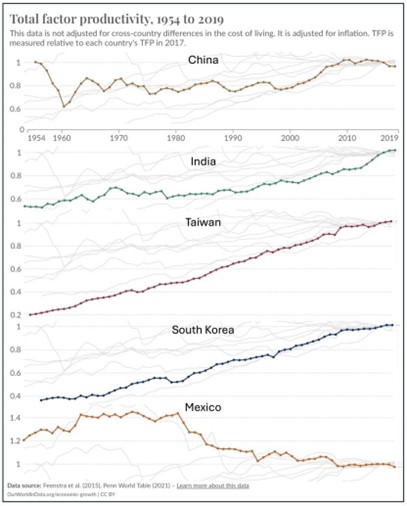

The 2008 unemployment crisis was managed, but China’s GDP at the time was under US$5 trillion—about a quarter of what it is today. The country’s manufacturing geographic footprint has expanded across all industries and is no longer contained within tightly clustered special economic zones along China’s eastern and southern coasts. And, not only has China’s economy grown exponentially over the past 16 years, so have the expectations of hundreds of millions more people who have migrated from a 19th-century rural agrarian lifestyle to a 21st-century city lifestyle.

EMPLOYMENT FIRST

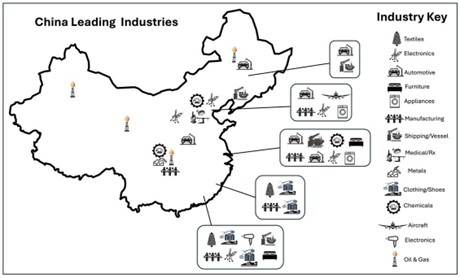

The crown jewel of China’s manufacturing prowess is its vertically integrated domestic supply chain—often having component makers just down the street, or another town over. This is a huge competitive advantage that makes for quick, accurate and competitive quotes, while adding manufacturing agility and cost savings. Example: component inventories can be low or zero for a final assembler if the component manufacturer is less than a half hour away.

competitive advantage that makes for quick, accurate and competitive quotes, while adding manufacturing agility and cost savings. Example: component inventories can be low or zero for a final assembler if the component manufacturer is less than a half hour away.

The imposition of tariffs by the United States largely negates this competitive advantage and Chinese manufacturers have responded by off-shoring downstream production. One destination is the Bamboo Network (Southeast Asia’s ethnic Chinese business network) countries. This avoids the US tariffs but leaves Ethnic Chinese ”Bamboo Network” Chinese manufacturers with diminished verticality in their upstream suppliers requiring large intermediate component inventories, added shipping costs and vastly extended lead-times.

The more clever and aggressive countries that aspire to join the manufacturer-to-the-world club are already busy decoding their formula for success and taking action. Pro-active rather than reactive strategies have drawn manufacturing to diverse countries ranging from Ireland to Costa Rica, which enjoys the highest GDP per capita in Central America after Panama.11To compete more aggressively and effectively in the scramble for manufacturing orders it is important to first take stock of Mexico’s strengths and weaknesses, and determine where it fits in a North American nearshoring model.

reactive strategies have drawn manufacturing to diverse countries ranging from Ireland to Costa Rica, which enjoys the highest GDP per capita in Central America after Panama.11To compete more aggressively and effectively in the scramble for manufacturing orders it is important to first take stock of Mexico’s strengths and weaknesses, and determine where it fits in a North American nearshoring model.

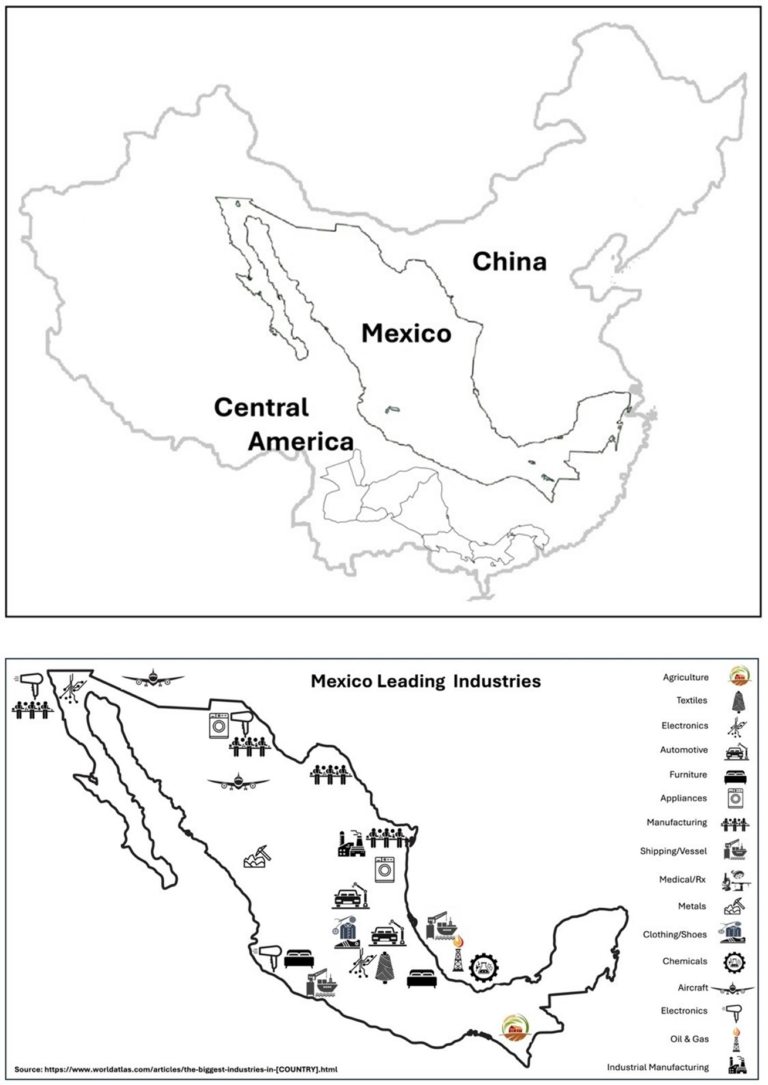

Mexico already enjoys a relatively respectable industrial base that is disbursed across the country. Mexico’s membership in NAFTA/USMCA has brought in manufacturing from North America, mainly in the form of OEM component manufacturing.

But the USA is also a member of CAFTADR FTA (Dominican Republic-Central AmericaUnited States Free Trade Agreement), which puts the entire geography from the US-Mexico border to the Panama-Columbia border under favored trade status. And these Central American countries bring their own capabilities to the table.

But the USA is also a member of CAFTADR FTA (Dominican Republic-Central AmericaUnited States Free Trade Agreement), which puts the entire geography from the US-Mexico border to the Panama-Columbia border under favored trade status. And these Central American countries bring their own capabilities to the table.

Taken as a whole, it is more practical for Mexico to see itself as a leading country within a regional economic zone—pursuing strategic specialization for acquiring a bigger share of the manufacturing vertical—than trying to become another China on its own. Most importantly, this region possesses two competitive advantages that China can never beat: adjacency to the United States and vastly lower national security concerns versus those about the CCP.